Interest income which makes up over 94% of total income, grew by 12% from UGX 1,605Bn in FY2020/21 to UGX 1,800Bn in FY2021/22. This was driven by the increased investment in government bonds.

Real Estate income declined by 22% from UGX 15.42Bn in FY2020/21 to UGX 11.97Bn in FY2021/22 due to low house sales compared to the prior year.

Dividend income grew by 33% from UGX 74.9Bn in FY2020/21 to UGX 99.8Bn in FY2021/22. This was driven by dividends from MTN and a general increase in dividends earned from Equity Group Holdings Ltd, Kenya Commercial Bank (KCB) and Cooperative Rural Development Bank (CRDB) Tanzania.

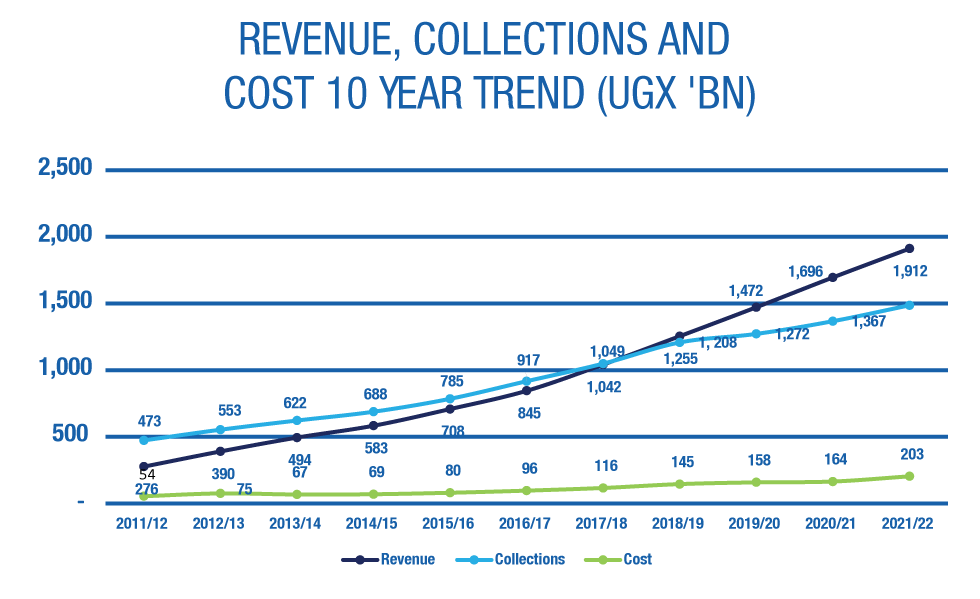

As a result, total realised revenue grew by 13% from UGX 1,696Bn to UGX 1,912Bn driven by the growth in Fixed Income and Dividend Income growth.

Revenue

Interest income which makes up over 94% of total income, grew by 12% from UGX 1,605Bn in FY2020/21 to UGX 1,800Bn in FY2021/22. This was driven by the increased investment in government bonds.

Real Estate income declined by 22% from UGX 15.42Bn in FY2020/21 to UGX 11.97Bn in FY2021/22 due to low house sales compared to the prior year.

Dividend income grew by 33% from UGX 74.9Bn in FY2020/21 to UGX 99.8Bn in FY2021/22. This was driven by dividends from MTN and a general increase in dividends earned from Equity Group Holdings Ltd, Kenya Commercial Bank (KCB) and Cooperative Rural Development Bank (CRDB) Tanzania.

As a result, total realised revenue grew by 13% from UGX 1,696Bn to UGX 1,912Bn driven by the growth in Fixed Income and Dividend Income growth.

Operating Costs

Annual operating costs amounted to UGX 203Bn, up by 24% from UGX 164Bn in FY2020/21 and 5% above the budget of UGX 194Bn. This was driven by the changes from the organisational redesign to align the Fund’s operations with the opportunities presented by the NSSF Amendment Act 2022 in addition to the general increase in prices of goods and services.

Consequently, the annual cost-to-income ratio stood at 11.4% in FY2021/22, up from 8.9% in FY2020/21. The expense ratio increased to 1.18% in FY2021/22 from 1.06% in FY2020/21. This was higher than the target of 1.15%.

Whereas revenue and collections have grown by a compound annual growth rate (CAGR) of 21% and 12% respectively, costs have only grown by a CAGR of 14% over a 10-year period (FY2011/12-FY2021/22). Revenue has posted significant growth over the historical period, and it surpassed collections from FY2018/19 onwards. In FY2021/22, revenue was higher than collections by 29% and this gap continues to grow.

Operating Costs

Annual operating costs amounted to UGX 203Bn, up by 24% from UGX 164Bn in FY2020/21 and 5% above the budget of UGX 194Bn. This was driven by the changes from the organisational redesign to align the Fund’s operations with the opportunities presented by the NSSF Amendment Act 2022 in addition to the general increase in prices of goods and services.

Consequently, the annual cost-to-income ratio stood at 11.4% in FY2021/22, up from 8.9% in FY2020/21. The expense ratio increased to 1.18% in FY2021/22 from 1.06% in FY2020/21. This was higher than the target of 1.15%.

Whereas revenue and collections have grown by a compound annual growth rate (CAGR) of 21% and 12% respectively, costs have only grown by a CAGR of 14% over a 10-year period (FY2011/12-FY2021/22). Revenue has posted significant growth over the historical period, and it surpassed collections from FY2018/19 onwards. In FY2021/22, revenue was higher than collections by 29% and this gap continues to grow.

Interest Credited to Members

The Fund declared a return to members of 9.65% in the FY 2021/22 resulting in UGX 1,380Bn compared to 12.15% in FY 2020/21 which resulted in UGX 1,516Bn. The decline in the return was due to the diminishing returns because of the reduction in the funds available for long-term investment. This was due to increased benefits pay-outs from midterm access and lower returns earned from undertaking shorter-term investments to meet the midterm access obligations.

Interest Credited to Members

The Fund declared a return to members of 9.65% in the FY 2021/22 resulting in UGX 1,380Bn compared to 12.15% in FY 2020/21 which resulted in UGX 1,516Bn. The decline in the return was due to the diminishing returns because of the reduction in the funds available for long-term investment. This was due to increased benefits pay-outs from midterm access and lower returns earned from undertaking shorter-term investments to meet the midterm access obligations.

Financial Position

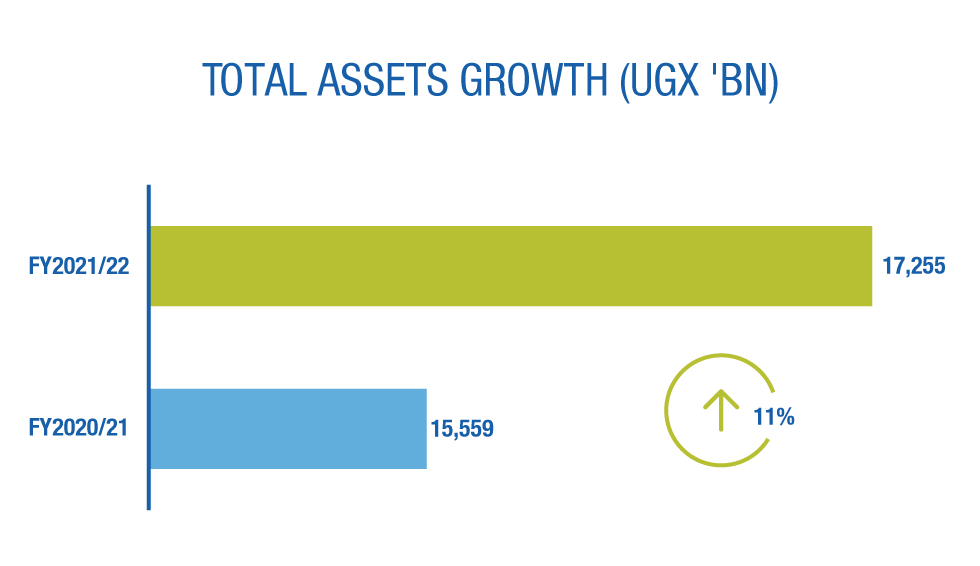

The Fund balance sheet size grew by 11% to UGX 17,255Bn (FY2020/21: UGX 15,559Bn).

This growth is consistent with the combined growth in investments driven by contributions and income generated net of benefits paid out.

The Fund invests in 3 asset classes: Fixed Income Securities, Equity Securities and Real Estate:

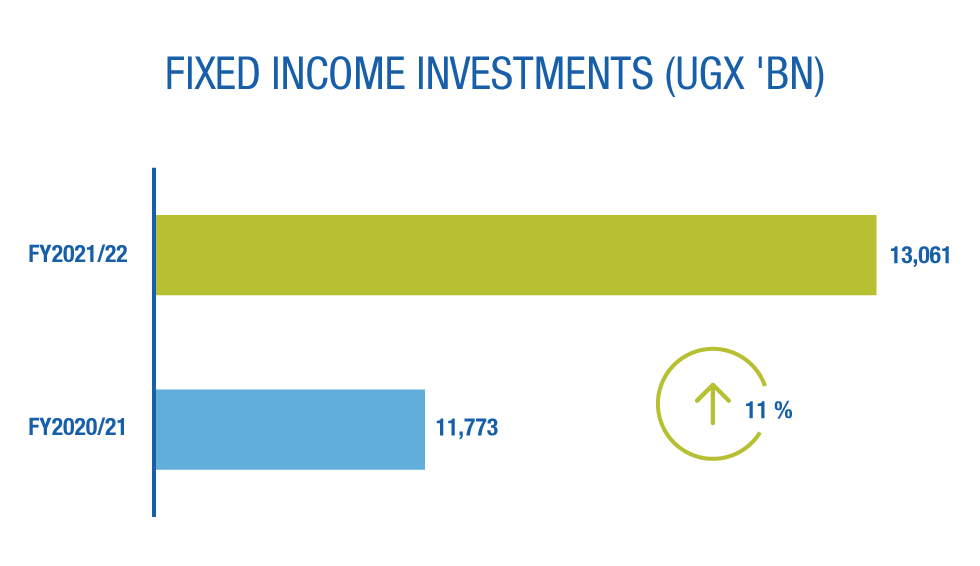

The 11% growth in Fixed Income investments to UGX 13,061Bn (FY2020/21: UGX 11,773Bn) was because of the increase in investment in government bonds in Uganda and Kenya.

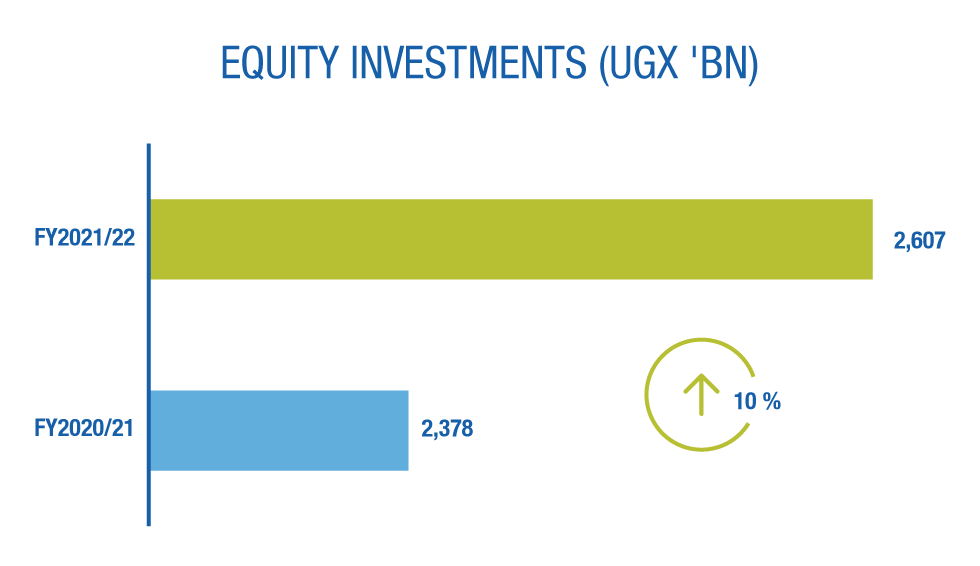

Equity Investments grew by 10% to UGX 2,607Bn (FY2020/21: UGX 2,378Bn) driven by investment in the MTN IPO.

Real Estate Investments grew by 4% to UGX 1,171Bn (FY2020/21: UGX 1,128Bn) due to progress achieved on ongoing projects including Pension Towers, Lubowa Housing Project, Bwebajja, and Kyanja.

Accumulated Member Fund

Member Fund grew by 11% to UGX 16,962Bn (FY2020/21: UGX 15,299Bn) driven by contribution collections of UGX 1,486Bn and interest credited to members of UGX 1,380Bn net of total benefits paid of UGX 1,189Bn.

Financial Position

The Fund balance sheet size grew by 11% to UGX 17,255Bn (FY2020/21: UGX 15,559Bn).

This growth is consistent with the combined growth in investments driven by contributions and income generated net of benefits paid out.

The Fund invests in 3 asset classes: Fixed Income Securities, Equity Securities and Real Estate:

The 11% growth in Fixed Income investments to UGX 13,061Bn (FY2020/21: UGX 11,773Bn) was because of the increase in investment in government bonds in Uganda and Kenya.

Equity Investments grew by 10% to UGX 2,607Bn (FY2020/21: UGX 2,378Bn) driven by investment in the MTN IPO.

Real Estate Investments grew by 4% to UGX 1,171Bn (FY2020/21: UGX 1,128Bn) due to progress achieved on ongoing projects including Pension Towers, Lubowa Housing Project, Bwebajja, and Kyanja.

Accumulated Member Fund

Member Fund grew by 11% to UGX 16,962Bn (FY2020/21: UGX 15,299Bn) driven by contribution collections of UGX 1,486Bn and interest credited to members of UGX 1,380Bn net of total benefits paid of UGX 1,189Bn.

Taxation

The Tax Appeals Tribunal ruled against NSSF in March 2020 in a significant income tax matter that has been under dispute since 2013. NSSF appealed to the High Court on 2 November 2020. The High Court delivered judgment in favour of the National Social Security Fund. The court ruled that the interest paid by the Fund to its members is a deductible expense for income tax purposes and that the Fund was not liable to pay the tax assessed. The Uganda Revenue Authority (URA) was dissatisfied with the decision of the High Court and subsequently filed an application for leave to appeal and an application for stay of execution.

On 16 August 2022, the High Court dismissed the application for leave to appeal with costs, citing that it was filed outside the statutory period envisioned under Rule 40(1) of the Judicature Court of Appeal Rules. The Court further ruled that a delay of 92 days was unreasonable and there was no proper reason for the delay.

Cashflow Analysis

The closing cash and bank balances stood at UGX 73Bn in FY2021/22 compared to UGX 81Bn in FY2020/21.

Net cash generated from financing activities amounted to UGX 309Bn. Net cash flows used in investing activities was UGX 175Bn whereas net cash flows used in operations was UGX 142Bn.

This is a clear indicator of the Fund’s ability to generate enough cash for all routine operations and investing activities.

Update on Accounting Standards

Due to the constantly evolving global business environment, the International Accounting Standards Board (IASB) which develops and approves International Financial Reporting Standards (IFRS) under the oversight of the IFRS Foundation, issued new standards and amendments to the existing ones.

Several amendments to existing standards became effective during the year. However, these had little/no impact on the Fund’s financial statements. These included the following:

Property, Plant and Equipment: Proceeds before Intended Use – Amendments to IAS 16-effective 1 January 2022.

Onerous Contracts: Costs of Fulfilling a Contract – Amendments to IAS 37 – effective 1 January 2022.

IFRS 9 Financial Instruments: Fees in the ’10 percent test for derecognition of financial liabilities.

IAS 41 Agriculture: Taxation in fair value measurements.

We highlight further the significant accounting policies and how these affect the Fund in Note 3 of the financial statements.

Taxation

The Tax Appeals Tribunal ruled against NSSF in March 2020 in a significant income tax matter that has been under dispute since 2013. NSSF appealed to the High Court on 2 November 2020. The High Court delivered judgment in favour of the National Social Security Fund. The court ruled that the interest paid by the Fund to its members is a deductible expense for income tax purposes and that the Fund was not liable to pay the tax assessed. The Uganda Revenue Authority (URA) was dissatisfied with the decision of the High Court and subsequently filed an application for leave to appeal and an application for stay of execution.

On 16 August 2022, the High Court dismissed the application for leave to appeal with costs, citing that it was filed outside the statutory period envisioned under Rule 40(1) of the Judicature Court of Appeal Rules. The Court further ruled that a delay of 92 days was unreasonable and there was no proper reason for the delay.

Cashflow Analysis

The closing cash and bank balances stood at UGX 73Bn in FY2021/22 compared to UGX 81Bn in FY2020/21.

Net cash generated from financing activities amounted to UGX 309Bn. Net cash flows used in investing activities was UGX 175Bn whereas net cash flows used in operations was UGX 142Bn.

This is a clear indicator of the Fund’s ability to generate enough cash for all routine operations and investing activities.

Update on Accounting Standards

Due to the constantly evolving global business environment, the International Accounting Standards Board (IASB) which develops and approves International Financial Reporting Standards (IFRS) under the oversight of the IFRS Foundation, issued new standards and amendments to the existing ones.

Several amendments to existing standards became effective during the year. However, these had little/no impact on the Fund’s financial statements. These included the following:

Property, Plant and Equipment: Proceeds before Intended Use – Amendments to IAS 16-effective 1 January 2022.

Onerous Contracts: Costs of Fulfilling a Contract – Amendments to IAS 37 – effective 1 January 2022.

IFRS 9 Financial Instruments: Fees in the ’10 percent test for derecognition of financial liabilities.

IAS 41 Agriculture: Taxation in fair value measurements.

We highlight further the significant accounting policies and how these affect the Fund in Note 3 of the financial statements.