The pandemic saw aggressive quantitative easing and stimulus packages in the developed world to stimulate economies. To take the example of the US, this was at about 18% of GDP. Presently, we are in an era of quantitative tightening after several years of quantitative easing in most of the developed world.

The Fed and the ECB have both raised rates in 2022 taking the benchmark rate in the US to a range of 2.25%-2.5% —expected at between 4%-4.25% by the end of 2022. In the EU, we are destined to see positive interest rates for the first time in 11 years with the benchmark trend expected at 2%-2.25% by the end of 2023. This has ramifications for our markets. Regional currencies will depreciate against the dollar, and this will result in imported inflation, most especially for the net importers. In any event, this process, and the emerging geopolitical tensions, will cause lots of consternation and very volatile markets. Yet today’s economic landscape is completely different from the 2008 financial crisis when the consumer in the world’s biggest economy was extraordinarily overleveraged, as was the financial system as a whole — from banks and investment banks to shadow banks, hedge funds, private equity, Fannie Mae, and many other entities.

During the fiscal year, the Uganda Shilling appreciated against Kenya Shilling, its major portfolio currency by 3.4%. However, it depreciated by 4.8% against Tanzania Shilling, 5.3% to the USD and 2.9% to the Rwandese Franc. This had a net impact of UGX 13.63Bn in currency losses.

The pandemic saw aggressive quantitative easing and stimulus packages in the developed world to stimulate economies. To take the example of the US, this was at about 18% of GDP. Presently, we are in an era of quantitative tightening after several years of quantitative easing in most of the developed world.

The Fed and the ECB have both raised rates in 2022 taking the benchmark rate in the US to a range of 2.25%-2.5% —expected at between 4%-4.25% by the end of 2022. In the EU, we are destined to see positive interest rates for the first time in 11 years with the benchmark trend expected at 2%-2.25% by the end of 2023. This has ramifications for our markets. Regional currencies will depreciate against the dollar, and this will result in imported inflation, most especially for the net importers. In any event, this process, and the emerging geopolitical tensions, will cause lots of consternation and very volatile markets. Yet today’s economic landscape is completely different from the 2008 financial crisis when the consumer in the world’s biggest economy was extraordinarily overleveraged, as was the financial system as a whole — from banks and investment banks to shadow banks, hedge funds, private equity, Fannie Mae, and many other entities.

During the fiscal year, the Uganda Shilling appreciated against Kenya Shilling, its major portfolio currency by 3.4%. However, it depreciated by 4.8% against Tanzania Shilling, 5.3% to the USD and 2.9% to the Rwandese Franc. This had a net impact of UGX 13.63Bn in currency losses.

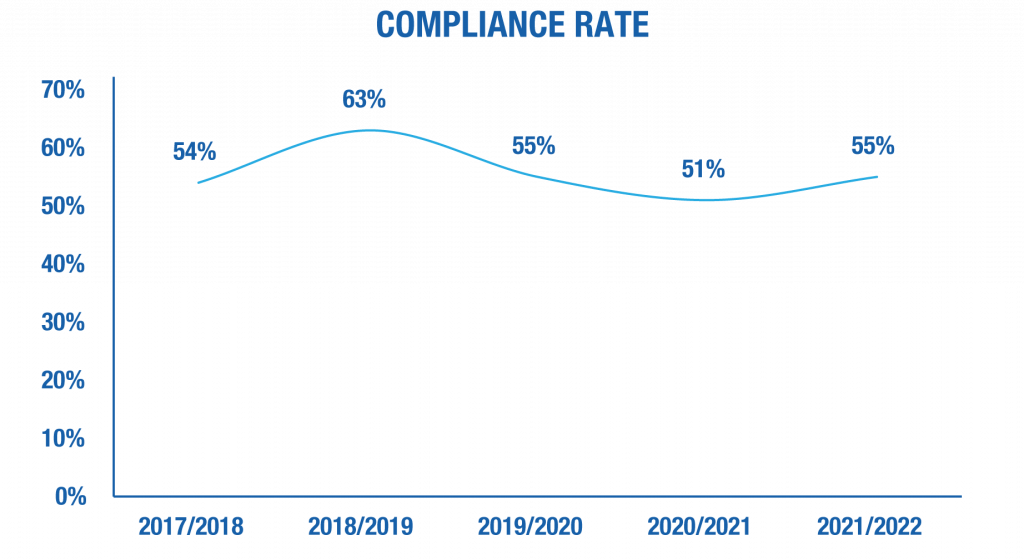

The impact of the lockdown to combat the spread of Covid-19 weighed heavily on compliance rates. But as depicted in Figure 3, we saw compliance rates recover (to the levels seen in 2019/2020) in the fiscal year.

This was attributed to the reopening of the economy. Despite the recovery in compliance, the contributions target was short by UGX 14Bn.

The trade-off was that with insufficient collections, the investment programme was affected.

Source: Internal

The impact of the lockdown to combat the spread of Covid-19 weighed heavily on compliance rates. But as depicted in Figure 3, we saw compliance rates recover (to the levels seen in 2019/2020) in the fiscal year.

This was attributed to the reopening of the economy. Despite the recovery in compliance, the contributions target was short by UGX 14Bn.

The trade-off was that with insufficient collections, the investment programme was affected.

Russia’s invasion of Ukraine and the ensuing sanctions added (and continue to add) another element of havoc to already stretched global supply chains and further volatility to jittery financial markets after Covid-19. This coupled with the dry weather conditions, has exacerbated inflation pressures in the region thereby risking a stagflation threat. Africa is not immune to the crisis as Russia and Ukraine are major producers of various key commodities such as oil, gas, wheat, and corn. Therefore, the imposition of sanctions and the disruption of the supply chains has led to soaring prices of commodities.

To this end, Central Banks must walk a tightrope: attempting to balance rampant inflation with policy tools such as rate increases, mindful of soaring commodity prices and stretched supply chains, while aiming for growth. This scenario is always more difficult for emerging/frontier markets, which are by nature more vulnerable to changes in rates and inflationary pressures. However, opportunities abound for adept stock pickers.

The escalation in construction materials prices because of disruptions in supply chains and rising fuel costs has affected projects. To this end, the progress on construction works slowed down as contractors requested either contract variations and/or extensions of time. The projects affected included Lubowa, Temangalo, Pension Towers, Mbale Commercial Development, and the Off-taker Project in Kyanja. We continue to navigate the bumpy path of balancing compliance while pragmatically solving the issues on the various projects to improve progress.

Russia’s invasion of Ukraine and the ensuing sanctions added (and continue to add) another element of havoc to already stretched global supply chains and further volatility to jittery financial markets after Covid-19. This coupled with the dry weather conditions, has exacerbated inflation pressures in the region thereby risking a stagflation threat. Africa is not immune to the crisis as Russia and Ukraine are major producers of various key commodities such as oil, gas, wheat, and corn. Therefore, the imposition of sanctions and the disruption of the supply chains has led to soaring prices of commodities.

To this end, Central Banks must walk a tightrope: attempting to balance rampant inflation with policy tools such as rate increases, mindful of soaring commodity prices and stretched supply chains, while aiming for growth. This scenario is always more difficult for emerging/frontier markets, which are by nature more vulnerable to changes in rates and inflationary pressures. However, opportunities abound for adept stock pickers.

The escalation in construction materials prices because of disruptions in supply chains and rising fuel costs has affected projects. To this end, the progress on construction works slowed down as contractors requested either contract variations and/or extensions of time. The projects affected included Lubowa, Temangalo, Pension Towers, Mbale Commercial Development, and the Off-taker Project in Kyanja. We continue to navigate the bumpy path of balancing compliance while pragmatically solving the issues on the various projects to improve progress.

Despite some of the downside effects and trade-offs, we took advantage of several opportunities:

Although the equity markets were volatile towards the end of the financial year, we took advantage of the diversification opportunities in the market. The MTN listing in December 2021 on the Uganda Securities Exchange saw the Fund invest UGX 360Bn thereby taking advantage of the local institutional investor allocation which resulted in an effective cost of UGX 182 per share, compared to the IPO price of Ush 200. The Fund now owns 8.8% of the company.

Despite our stretched liquidity situation, we took advantage of the bearish market sentiment which offered some good entry positions in other regional equities. The activity was unprecedented in a single fiscal year leading to the deployment of UGX 419Bn in equities—this includes MTN. We believe this puts the Fund in a good place to take advantage of the recovery of the markets when it does happen—we believe this will happen in not more than two years. Equally, this gives credence to the investment strategy that we have adopted over the years: taking advantage of the regional market opportunities to achieve diversification of the portfolio. It is a continuous journey.

The result is that over the years, we have managed to build resilience in the overall portfolio performance, irrespective of the times—2022 being another testimony to that.

Recession fears dampen emerging/frontier market duration demand, with foreign investors unloading their exposure. Kenya Eurobonds were no exception. The situation was worsened by the political risk which led to the cancellation of the planned issuance of the Eurobond. This saw yields climbing to 20%, an ideal opportunity to gain exposure, which we took advantage of.

Despite some of the downside effects and trade-offs, we took advantage of several opportunities:

Although the equity markets were volatile towards the end of the financial year, we took advantage of the diversification opportunities in the market. The MTN listing in December 2021 on the Uganda Securities Exchange saw the Fund invest UGX 360Bn thereby taking advantage of the local institutional investor allocation which resulted in an effective cost of UGX 182 per share, compared to the IPO price of Ush 200. The Fund now owns 8.8% of the company.

Despite our stretched liquidity situation, we took advantage of the bearish market sentiment which offered some good entry positions in other regional equities. The activity was unprecedented in a single fiscal year leading to the deployment of UGX 419Bn in equities—this includes MTN. We believe this puts the Fund in a good place to take advantage of the recovery of the markets when it does happen—we believe this will happen in not more than two years. Equally, this gives credence to the investment strategy that we have adopted over the years: taking advantage of the regional market opportunities to achieve diversification of the portfolio. It is a continuous journey.

The result is that over the years, we have managed to build resilience in the overall portfolio performance, irrespective of the times—2022 being another testimony to that.

Recession fears dampen emerging/frontier market duration demand, with foreign investors unloading their exposure. Kenya Eurobonds were no exception. The situation was worsened by the political risk which led to the cancellation of the planned issuance of the Eurobond. This saw yields climbing to 20%, an ideal opportunity to gain exposure, which we took advantage of.

Responsible investment is an integral part of the Fund’s investment thesis. We aim to identify long-term investment opportunities to reduce the Fund’s exposure to unacceptable risks. Climate change is a major risk and mitigating it is the responsibility of all. The steady convergence of evidence, opinion, commitments and action among governments, corporations and civil society concerning the need to transition the global economy to a low-carbon future, identified broadly as “net zero by 2050,” has added impetus to our collective responsibility to act. But we do this pragmatically.

In most of our equity investment decision-making, to the extent possible, we assess how companies impact the environment, society, and opportunities. We look at companies that enable more environmentally friendly economic activity favourably. Through our active engagement model, we can directly engage with our portfolio companies on a wide range of material ESG-related considerations to enhance their long-term value to the Fund. We align these efforts to the value drivers of our portfolio companies, tailoring our approach to connect the issues that are most material to the companies’ long-term value creation and preservation.

There are also companies we may choose not to invest in for sustainability or ethical reasons, for example, tobacco companies. On the other hand, we see merit in investing in companies with solutions that enable more environmentally friendly economic activity and sustainability. These investments can have positive effects on other companies in the portfolio. These positive externalities can include reduced pollution, lower energy costs and more efficient use of resources.

Our top five (5) equity holdings depicted in Table 2 below constitute 53.4% of the equity portfolio and are strong on sustainability through foundations focusing on themes like; economic empowerment, education, health, energy and the environment, food and agriculture, social protection, to mention but some. When we track all companies in the equity portfolio that are strong on sustainability, they constitute about 74% of the equity portfolio.

| Number | Counter | Amount (UGX) | % |

|---|---|---|---|

|

1 |

MTN |

352,618,200,000 |

14.60% |

|

2 |

SAFCOM |

299,227,958,673 |

12.40% |

|

3 |

TBL |

224,498,919,236 |

9.30% |

|

4 |

EQBNK |

210,300,939,628 |

8.70% |

|

5 |

KCB |

201,854,604,859 |

8.40% |

|

6 |

TDB |

168,361,710,832 |

7.00% |

|

7 |

CRDB |

126,902,977,436 |

5.30% |

|

8 |

Stanbic Bank Uganda |

46,271,201,812 |

1.90% |

|

9 |

NMB Bank (NMB TZ) |

117,900,619,200 |

4.90% |

|

10 |

Vodacom (VODA) |

34,589,526,790 |

1.40% |

|

11 |

Serena Hotel |

7,134,287,355 |

0.30% |

|

12 |

Yield Fund |

2,321,844,000 |

0.10% |

|

Total |

1,791,982,789,821 |

74.30% |

|

Responsible investment is an integral part of the Fund’s investment thesis. We aim to identify long-term investment opportunities to reduce the Fund’s exposure to unacceptable risks. Climate change is a major risk and mitigating it is the responsibility of all. The steady convergence of evidence, opinion, commitments and action among governments, corporations and civil society concerning the need to transition the global economy to a low-carbon future, identified broadly as “net zero by 2050,” has added impetus to our collective responsibility to act. But we do this pragmatically.

In most of our equity investment decision-making, to the extent possible, we assess how companies impact the environment, society, and opportunities. We look at companies that enable more environmentally friendly economic activity favourably. Through our active engagement model, we can directly engage with our portfolio companies on a wide range of material ESG-related considerations to enhance their long-term value to the Fund. We align these efforts to the value drivers of our portfolio companies, tailoring our approach to connect the issues that are most material to the companies’ long-term value creation and preservation.

There are also companies we may choose not to invest in for sustainability or ethical reasons, for example, tobacco companies. On the other hand, we see merit in investing in companies with solutions that enable more environmentally friendly economic activity and sustainability. These investments can have positive effects on other companies in the portfolio. These positive externalities can include reduced pollution, lower energy costs and more efficient use of resources.

Our top five (5) equity holdings depicted in Table 2 below constitute 53.4% of the equity portfolio and are strong on sustainability through foundations focusing on themes like; economic empowerment, education, health, energy and the environment, food and agriculture, social protection, to mention but some. When we track all companies in the equity portfolio that are strong on sustainability, they constitute about 74% of the equity portfolio.

| Number | Counter | Amount (UGX) | % |

|---|---|---|---|

|

1 |

MTN |

352,618,200,000 |

14.60% |

|

2 |

SAFCOM |

299,227,958,673 |

12.40% |

|

3 |

TBL |

224,498,919,236 |

9.30% |

|

4 |

EQBNK |

210,300,939,628 |

8.70% |

|

5 |

KCB |

201,854,604,859 |

8.40% |

|

6 |

TDB |

168,361,710,832 |

7.00% |

|

7 |

CRDB |

126,902,977,436 |

5.30% |

|

8 |

Stanbic Bank Uganda |

46,271,201,812 |

1.90% |

|

9 |

NMB Bank (NMB TZ) |

117,900,619,200 |

4.90% |

|

10 |

Vodacom (VODA) |

34,589,526,790 |

1.40% |

|

11 |

Serena Hotel |

7,134,287,355 |

0.30% |

|

12 |

Yield Fund |

2,321,844,000 |

0.10% |

|

Total |

1,791,982,789,821 |

74.30% |

|

We are also on course to getting the Green Building Certification for the Pension Towers project—expected to be completed in 2023, and the Temangalo Housing Project—expected to be completed in 2024. Moreover, we aim to reduce energy costs by about 10% in the next two years using automatic lighting systems, energy-efficient fittings/ appliances, and prepaid meters on the properties we manage like; Workers House, Social Security House, Jinja and Mbarara City Buildings.

The hardest part is measuring impact. Going forward, as part of our sustainability story, the Fund will be tracking and measuring the non-financial return which will be shared as part of financial reporting. This is expected for the fiscal year 2022/2023.

We are also on course to getting the Green Building Certification for the Pension Towers project—expected to be completed in 2023, and the Temangalo Housing Project—expected to be completed in 2024. Moreover, we aim to reduce energy costs by about 10% in the next two years using automatic lighting systems, energy-efficient fittings/ appliances, and prepaid meters on the properties we manage like; Workers House, Social Security House, Jinja and Mbarara City Buildings.

The hardest part is measuring impact. Going forward, as part of our sustainability story, the Fund will be tracking and measuring the non-financial return which will be shared as part of financial reporting. This is expected for the fiscal year 2022/2023.